Highlights

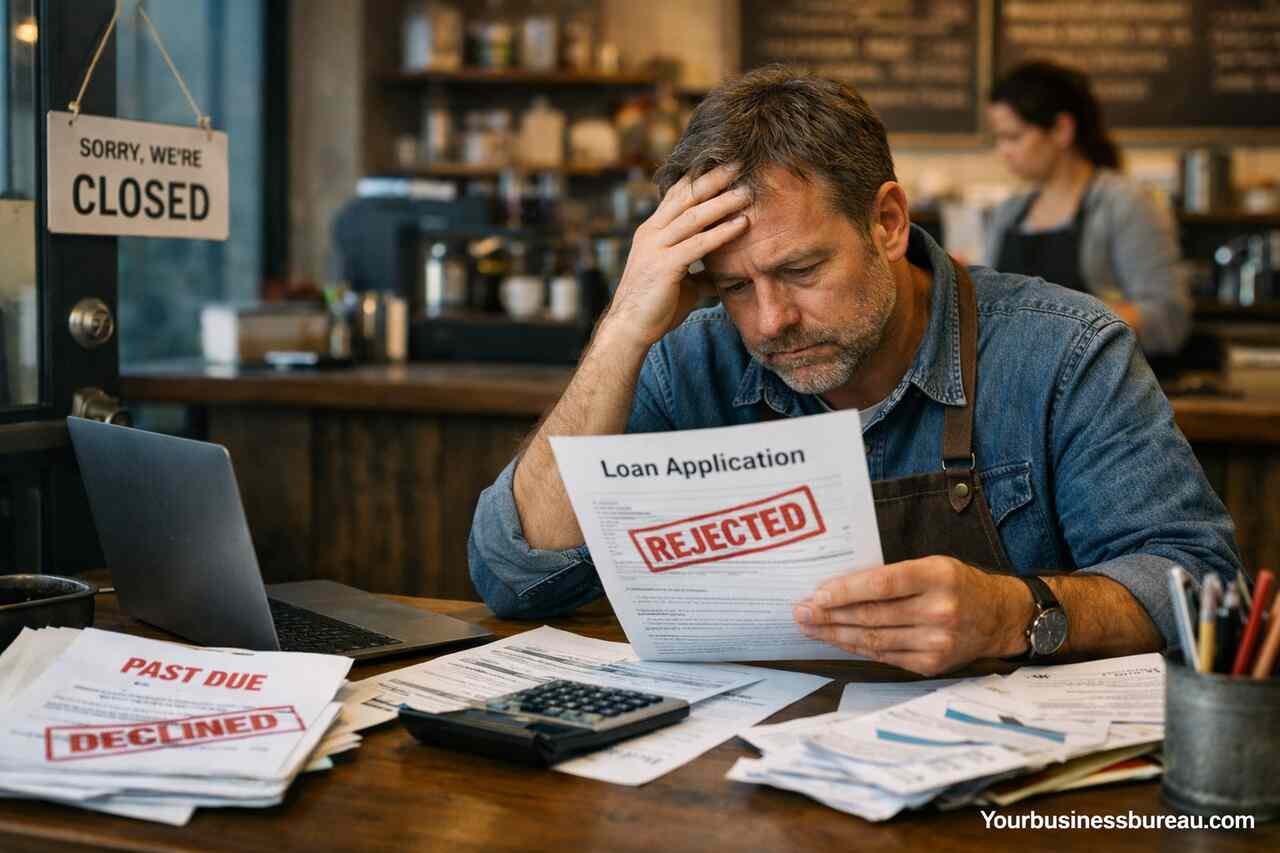

- You built a great business idea, but your loan got denied.

Even strong business models can be rejected if your documents are incomplete or your numbers aren’t consistent.

- You applied confidently, but your personal credit pulled you down.

Lenders heavily weigh your personal financial history, especially when business credit is still limited.

- You thought being in business for a year was enough.

Most banks want 2–3 years of operational history to trust your stability and revenue patterns.

- Your profits looked good, but your cash flow said otherwise.

Inconsistent cash flow or high expenses can signal risk even if your annual revenue is solid.

- You picked a loan, but not the right lender.

Not all loans fit your business stage. Traditional banks, SBA, and fintechs all have different requirements.

- You rushed your application and skipped the strategy.

Vague loan purposes and poor presentation can instantly ruin your chances, even with good financials.

- You tried again, but didn’t fix what went wrong.

Success happens when you audit your finances, rebuild credit, and approach the right lender with a clear plan.

Introduction

Navigating the financial system as a small business owner in the United States often brings a set of challenges, especially when applying for loans. Many entrepreneurs experience frustration when loan applications are denied, leaving them without the funding needed to grow or even survive. Through my own conversations with small business owners, and having gone through the process myself, I’ve seen firsthand how complex and discouraging the rejection process can be. This article explores the key reasons behind loan rejections and offers practical insights into how to overcome those hurdles. Whether you’re a startup owner or managing an established local business, understanding the barriers is the first step to financial readiness.

Why Do Small Businesses in the Us Face Funding Rejection Despite Market Demand?

Many small businesses are denied loans not because their ideas lack potential but due to financial and structural weaknesses. Lenders focus on risk. If your business doesn’t meet the defined risk thresholds, approval becomes unlikely. I’ve been in conversations with bankers who told me outright that even a strong business model can get overlooked if numbers and paperwork don’t align with underwriting standards.

The loan evaluation process doesn’t always consider innovation or growth trends in your industry. Instead, credit history, repayment capacity, and documentation become the priority. Even if your business has strong market traction, banks may deny you based on outdated or inconsistent financial records. That’s why it’s not enough to be good at what you do. You have to prove it through numbers.

Another hidden problem I’ve seen is that many small businesses underestimate the importance of strategic financial presentation. It’s not just about how much you make. It’s about how well you can show sustainability, profit consistency, and operational discipline. Many entrepreneurs don’t realize they’re seen as high-risk even if revenue looks promising on paper.

Inadequate Financial Documentation

Many business owners fail to present complete and accurate financial documents. Lenders require tax returns, profit and loss statements, and cash flow records. Missing or inconsistent documents often signal poor financial management, causing automatic rejections from traditional lenders.

Lack of Collateral

Traditional lending often requires physical or financial assets as security. Many small businesses, especially service-based or digital startups, lack tangible collateral. This increases the lender’s risk perception and limits access to secured loan options.

How Does Credit History Influence Loan Decisions for Small Businesses?

Credit history serves as the foundation for trust in the lending relationship. During my own application process, I was shocked at how much weight the personal credit score carried. Even though my business was profitable, a dip in my personal score significantly affected loan eligibility. Lenders assume that past behavior reflects future reliability.

For many small business owners, personal and business finances are intertwined. A missed credit card payment from years ago, or an unresolved account from a previous business, can influence how underwriters assess your current credibility. Even minor delinquencies can result in a “decline” decision.

Beyond credit score, the credit mix, utilization rate, and length of credit history all matter. A business with little credit history or one that relies heavily on revolving credit can be flagged as high-risk. I’ve talked to entrepreneurs who were doing well operationally but were turned away simply for lacking credit depth.

Low Personal Credit Score

Lenders often treat small business loan applications as personal risk decisions. A credit score below 650 can result in immediate disqualification, especially from traditional banks. Improving personal credit is often the fastest route to loan approval.

Thin Business Credit Profile

A business without established credit lines or trade accounts might not meet the threshold for institutional lending. Building vendor relationships and using business credit cards wisely help strengthen this profile over time.

What Role Does Business Age and Operational History Play in Loan Rejection?

New businesses face a steep climb when applying for funding. I remember when I first launched my own company. Just hitting the 12-month mark didn’t magically open the doors to financing. Banks and lenders want to see at least 2 to 3 years of stable operation before considering significant funding.

The reasoning is simple. Longer operational history equals lower perceived risk. Lenders look for patterns of revenue, customer retention, and expense control over time. Startups or recently incorporated businesses often lack this track record and are seen as unproven.

Even if a business is technically two years old, inconsistent income or seasonal revenue dips can be interpreted as instability. Many founders overlook the importance of consistency and assume occasional growth spikes will be enough to prove value. Unfortunately, that’s not how underwriters think.

Under Two Years in Operation

Businesses younger than 24 months are often automatically excluded from many bank loan programs. Alternative lenders may consider them but typically offer high-interest rates due to the perceived risk.

Inconsistent Revenue History

Fluctuating income, even during periods of overall growth, signals potential problems in sales strategy, customer loyalty, or cost control. Lenders prefer businesses with steady month-over-month revenue stability.

Why Do Cash Flow Issues Lead to Loan Application Denials?

Cash flow represents the real-time ability to cover liabilities and debts. I once reviewed my own application and noticed how even with strong annual revenue, inconsistent cash flow nearly tanked the process. Lenders aren’t just looking for sales. They want to see liquidity and cash availability.

Negative or uneven cash flow suggests that your business may struggle to meet loan repayments. Even if annual profit looks decent, a few slow months can raise red flags. I’ve advised fellow business owners to monitor cash flow statements weekly because banks closely examine this metric.

Inadequate cash flow planning often stems from poor forecasting or uncontrolled expenses. Lenders examine bank statements to identify spending patterns. A business with frequent overdrafts, bounced checks, or irregular deposits will usually be declined without further review.

High Operating Expenses

When a business’s fixed and variable costs take up too much of the revenue, the net cash flow suffers. High rent, payroll, or vendor payments can reduce the buffer needed to secure and repay loans.

Seasonal Revenue Gaps

Retailers and service providers often experience off-peak seasons. Without reserves or a secondary income stream, those gaps create repayment risks. Lenders prefer businesses with financial planning to bridge these periods.

How Do Loan Types and Lender Requirements Impact Rejection?

Each lender and loan type carries unique qualification criteria. I’ve personally been declined for a bank loan but approved by an online lender days later. The key difference was in how the two lenders evaluated risk and documents. Understanding lender expectations is critical.

Traditional banks demand extensive paperwork, high credit scores, and long operational history. SBA-backed loans add another layer of scrutiny. Meanwhile, fintech lenders may offer faster access with less paperwork but charge higher interest rates. Knowing which loan type aligns with your current position can save you from unnecessary rejections.

Some business owners apply blindly without aligning their profile to the loan’s purpose. A working capital loan and an equipment loan have different approval metrics. Misalignment between loan intent and financial documentation causes unnecessary denials.

Traditional Bank Loans

These loans offer lower interest rates but require the highest level of documentation and creditworthiness. Businesses lacking formal bookkeeping or collateral typically fail to meet requirements.

Online and Alternative Lenders

These lenders offer speed and flexibility but often come with higher costs and shorter terms. They cater to businesses with weaker credit or limited history but still evaluate bank statements and daily balances.

What Behavioral or Strategic Mistakes Cause Application Failures?

Beyond the numbers, strategic missteps often lead to rejections. I’ve seen businesses with healthy revenue get turned away simply because the owners didn’t articulate a clear repayment plan. Lenders expect clarity in both communication and planning.

Poorly prepared loan applications, vague business plans, or lack of loan purpose all signal disorganization. Lenders want to know exactly how the funds will be used and how repayments will be managed. A strong application tells a story backed by numbers.

Another critical mistake is applying too early or too often. Multiple applications in a short time can hurt your credit score and signal desperation. Instead, focus on one strong, tailored application. That approach significantly improved my own chances after two rejections.

Vague Loan Purpose

Lenders need assurance that the loan will contribute to revenue or operational growth. Vague purposes like “general use” or “just need capital” can signal poor planning or impulsive borrowing.

Poor Application Packaging

A well-prepared application includes clean financial statements, a business plan, and a repayment strategy. Incomplete or rushed submissions rarely make it past underwriting reviews.

How Can Small Businesses Improve Approval Chances for Future Loans?

Securing funding is not about luck. It’s about strategy, preparation, and consistency. After being rejected once, I overhauled my financial records, improved my credit score, and sought mentorship. Within six months, I secured a mid-range loan with favorable terms.

Improvement starts with internal controls. Regular financial audits, automated accounting tools, and financial literacy training can position any business for stronger applications. Avoiding late payments and optimizing cash reserves also play a huge role in reshaping your profile.

Finally, relationship-building with lenders matters. Regular communication with your bank, submitting quarterly updates, or even asking for pre-qualification advice helps build trust. A well-informed lender is more likely to support your business journey.

Upgrade Financial Systems

Use cloud-based accounting software to generate real-time reports. Clear, consistent records demonstrate financial control and improve credibility during loan reviews.

Build Lender Relationships

Stay connected with local banks, credit unions, and financial advisors. Networking allows better alignment with lender expectations and often leads to tailored funding opportunities.

What Steps Should Businesses Take Before Applying for a Loan?

Preparation makes the difference between approval and rejection. One of my biggest breakthroughs came when I spent 30 days just preparing for the application. Cleaning up credit, finalizing financial statements, and pre-drafting my loan proposal made all the difference.

Start by reviewing your credit reports and fixing errors. Then, generate at least 12 months of clean financial records. Make sure your tax filings are up to date and your debt-to-income ratio is healthy. These foundational elements build the case for approval.

Also, define exactly how you’ll use the funds and how they will contribute to measurable growth. Banks and lenders want to see not just repayment potential, but also a logical return on their investment. Proving that upfront shortens approval time and improves offer quality.

Review and Strengthen Credit Reports

Check for inaccuracies, disputes, or outdated accounts. Address delinquencies and pay down high balances to improve both personal and business credit profiles.

Draft a Specific Loan Strategy

Clearly outline how much capital you need, where it will be allocated, and what the projected returns will be. Attach this strategy to your loan application for a more compelling case.

Conclusion

Loan rejection is not a personal failure. It’s a systems-based decision that can be reversed with the right approach. I’ve been there myself, and I know how frustrating it can be to face rejection after investing years in your dream. By understanding the key factors that lenders evaluate such as credit history, operational track record, cash flow, and documentation, small businesses can position themselves more effectively. Future funding success depends on preparation, communication, and consistency. When these elements align, lenders are far more likely to say yes.

If you want to explore how we help businesses grow from the ground up, you can visit yourbusinessbureau.com to see what we offer.

FAQ’s

Most small businesses are closely tied to the owner’s financial behavior. Lenders view personal credit as a predictor of business loan repayment risk.

Yes, but usually through online or fintech lenders. These loans may come with higher interest rates and shorter terms compared to traditional options.

Reducing unnecessary expenses, negotiating longer payment terms with vendors, and increasing average transaction value can all help improve cash flow.

Yes, applying for multiple loans in a short time can hurt your credit score and make you appear financially unstable to lenders.

Tax returns, profit and loss statements, cash flow statements, bank records, and a business plan are typically the most critical.

Most traditional lenders prefer at least two years of consistent operation with verifiable revenue and profit history.